How to make a budget for beginners: From $11.75/hr in Toronto to Debt-Free by Thirty

- Blair Mueller

- 15 hours ago

- 5 min read

In 2005, I was living in Toronto, going to school full-time and working part-time for exactly $11.75 an hour. I wasn’t just "getting by"; I was drowning in the weight of tuition, student loans, and credit card debt while trying to figure out how to keep a roof over my head in one of the most expensive cities in Canada. I lived through a rough period I refer to as "the oatmeal days", and I was often scrounging around for pennies to make change for lunch.

It took years of jumping from job to job until I finally earned just over $20 an hour, but the real breakthrough wasn't the raise—it was the system I built to manage it. That system is what allowed me to stand tall and be debt-free by thirty.

Why "personal finance basics" aren't enough

When most people search for "how to make a budget for beginners", they are looking for a way out of the 14-day payday trap, what I call the "Tunnel Vision Financial Prison". We’ve all been there: that frantic cycle where you feel rich on Friday and bankrupt the following week. The problem is that most traditional advice is too rigid; it’s a "thou shalt not" list that makes you feel like a prisoner in your own life. They often set unrealistic goals like, you must spend 15% of your income on A, and you must never spend more than 40% of your income on B. But reality doesn't work like that. By those standards, I'd have been living in a shoebox with three other people for 16 years, not thriving in my own two bedroom apartment with a fridge full of food after paying off nearly $40k in debt by the age of 30. Facts!

To get out of the hole, you have to start with a mental demolition. You need to change how you view your money. It’s not just "cash"—it’s your life-force. No budget or "system" will work if you don't' change your mindset first.

Every time you fall for a "limited-time sale" or a marketing scheme, you’re letting someone else dictate where your life-force goes. Building marketing immunity is your first line of defense, especially in a world of convenience where corporations pay people billions of dollars a year to psychologically manipulate us into giving them more and more and more of our money using marketing schemes and tactics, preying on our weak minds, insecurities, and anxieties.

It’s about realizing that "saving $50" on something you didn't need is actually just spending $50 you didn't have. It's about realizing that "credit" is not money. It's just more debt. It's about identifying the invisible thief (interest... the rent you pay to carry a debt) and understanding exactly how that works.

The mental demolition phase of my course is about facing reality, seeing it for what it is, and making the decision to change your mindset and do things a bit differently than the societal norm. If you just do what everyone else is doing, and everyone else is also failing, why would you keep doing what everyone else is doing? Sometimes you have to go against the status quo.

How to save money on a low income (without losing your mind)

If you’re working with a smaller shovel, you have to be a better architect. You don't need a static, boring monthly budget template that breaks the moment life happens. You need a fluid system that lets you see the "bigger picture."

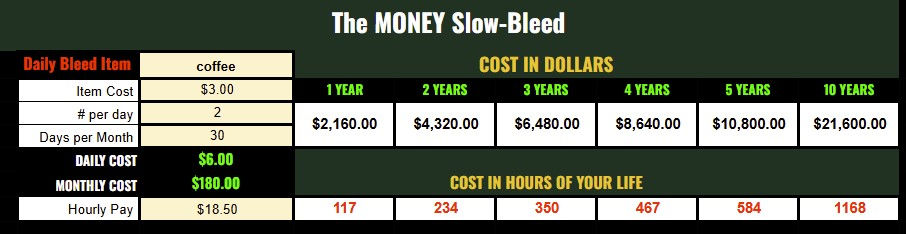

The secret to finding "hidden money" isn't usually in some massive lifestyle overhaul—it's in stopping the slow bleeds. These are the small, repetitive leaks like forgotten subscriptions, "convenience" fees in your daily life choices, and small buys that quietly drain your reservoir.

For example, I built a tool called "The Slow-Bleed Projection Gauge". It shows you exactly how much of your life-force you are giving away for something that, in the moment, seems like it's "no big deal." Did you know that buying 2 coffees a day could add up to the total of your entire debt load over the course of 5 years?

Here's a screenshot of part of this tool:

Here is the strategy:

Expose the Leaks: Look at your last 30 days. Find every charge that didn't actually add value to your life. Every subscription you paid to scroll through and endless stream of movies you'll never watch. Every small daily buy that you could make at home yourself for a tiny fraction of the cost. Essentially, you're identifying the "convenience fees" of your life.

Shift the Horizon: Stop looking at just the next two weeks. You need to see the next 12 months, 2 years, 5 years. To get out of the 14-day cycle, you need to look beyond next payday.

Build a Buffer: Even on a low income, protecting just $5 or $10 a week creates a psychological "foundation" that proves you are in control, not some marketing executive with a $3M home telling you all the reasons why you must give him another $15 a month to have something delivered to your doorstep.

Visualizing the 12-Month Build

In my course, I created the "mother of all spreadsheets" called The 12-Month Forecast Engine.

It doesn't just track your spending; it predicts your future. It shows you exactly when your foundation is stable and when an alarm is about to go off. It's the tool I have used for over almost two decades to navigate life in the most expensive city in Canada, paying off piles of debt, a global pandemic, paying off a car in under 2 years, and a 1.5 year battle with cancer. None of which caused financial collapse, because I have a solid system in place.

The Solution: Deploying the Blueprint

I won't lie to you: paying off debt is hard work. It takes dedication, a bit of grit, and a system that actually works in the real world. My course, The Debt Architect, was built from the very tools I used to clear $40k in debt while living alone in Toronto.

I’ll show you step-by-step how to find that hidden money and decrease your expenses without necessarily sacrificing the things you love. We aren't building a cage; we’re building a bridge to your Freedom Date.

If you’re tired of the "tunnel vision financial prison" and ready to see the whole site plan, I’ve got the machinery ready for you.

Clicking this icon takes you to the product page where you can add my course to your basket and check out in my store.

Comments